Thungela Resources Limited

Quick Thesis:

The thesis on Thungela is simple, if coal prices stay remotely close to what they are today the company will pretty much be printing off money thanks to its operating leverage. I expect the company to be at least a double within the next year as it declares its first dividend, has great earnings, and spinoff selling pressure continues to wear off.

Business Summary:

As previously stated, Thungela is a producer of coal through the operation of its seven coal mines in South Africa. The company is a very recent spinoff of American Anglo plc and is listed on the London and Johannesburg stock exchange at a market cap of around 8.3 billion rand. As with many mining companies, Thungela enjoys a very high degree of operating leverage which will be magnified given today’s high coal prices.

Looking more towards some of the downside of the company are its environmental liabilities which led a group named Boatman Capital to short the stock calling the company worthless. While I believe this is hyperbole (Boatman exited their short a long ways away from 0), in the risk section of this report I have modeled for some different scenarios including Boatman’s scenario in which the company’s liabilities are around 19 billion rand as opposed to the company reported 6.5 billion rand.

Finally, regarding the future demand of coal, it is very clear that richer nations are and will continue to reduce their use of coal as an energy source. Although this is definitely not something positive for the coal industry I still believe that for at least the next 40-50 years coal will be a source of energy and electric generation throughout the world. Global energy consumption is expected to grow by 22% (EnerOutlook2050) to 50% (EIA) based on different projections. No one can really nail it down to an extremely accurate number but the important takeaway is that energy consumption will increase and that it will come from developing regions such as Asia and more specifically developing countries such as India and South Africa. While I can’t say what the price of coal will be 3 or 8 years from now, I think that Thungela will likely still be around and have a viable business given coal prices do not plummet to the ground (total costs for exportable production is around 862 rand/t or around 58$). That being said I do not intend to hold the company for that long as I think it will rerate much faster.

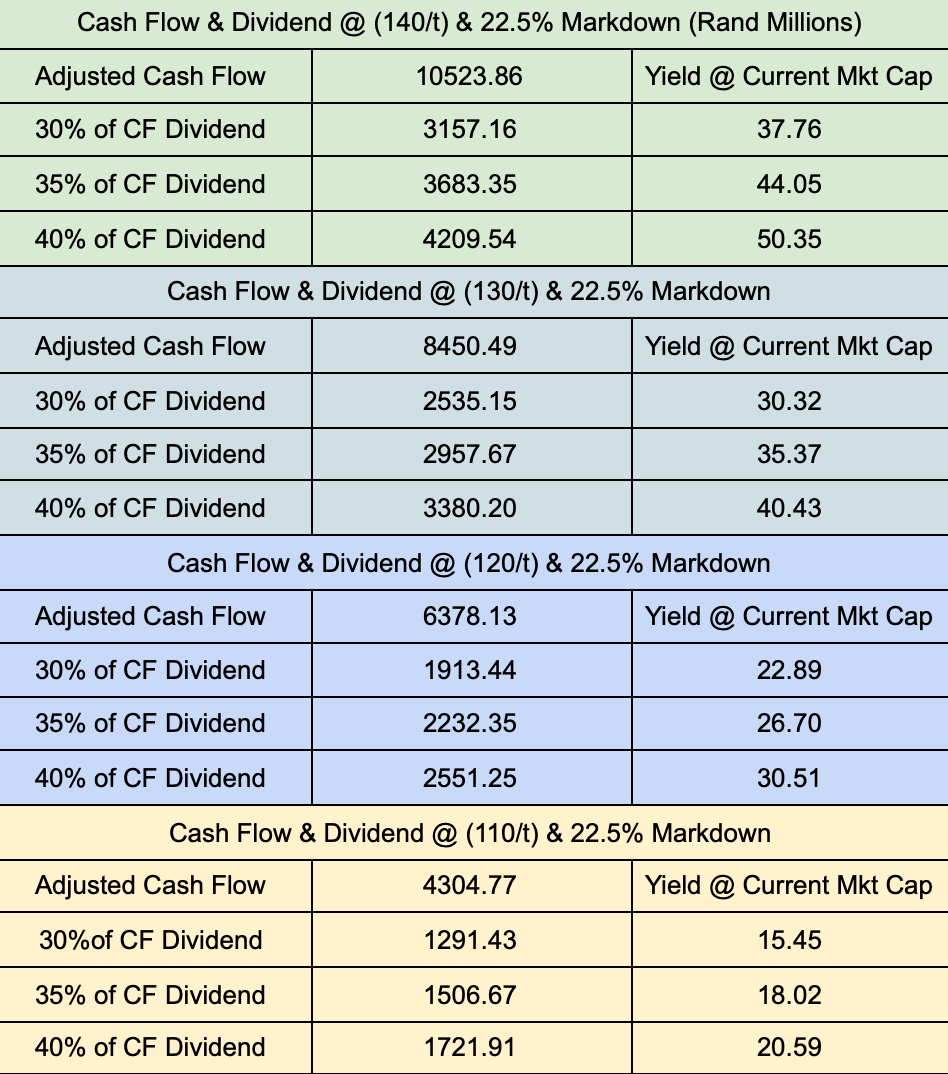

Valuation:

Regarding valuation, this company is dirt cheap. Based on 2022 mine by mine projected capex and production levels the company will easily produce 5-8 billion in rand. This is pretty conservative in my opinion and is modeling prices of around 120/ -130/t with production levels of around 19 million export tons of coal. As a result of a mine being put on maintenance and problems relating to rail transportation the company only produced 7.5 million tons of export sales in H1 2021. I think this will recover through H2 2021 and 2022 and I think 2022 levels while not quite being at 19 million will still be close to that number. This should be mitigated by the fact that coal prices have risen all the way to 155/t since I did my modeling for Thungela. Given 8 million exportable tons along with an average realized coal price of 140/t which at this point seems low Thungela will still bring in around 4 billion rand (of which the company has declared a minimum of 30% to be paid out as a dividend) in cashflow during H2 2021. This equates to a 29 percent annualized dividend that at a 10% rerate puts the company at around a 24 billion market cap or around 3x its current 8.4 billion rand market cap. When it comes to cheapness I can’t think of something much better than double and even possibly three digit free cash flow yields which is exactly what Thungela presents; given its current business prospects and impending catalysts Thungela is displaying a clearly massive value gap that should be closed on within the upcoming reporting periods.

Risks:

- Coal Prices

- Rail problems in South Africa may prevent the company from completely maxing out their sales at current prices.

-Environmental Liabilities: As pointed out by Boatman Capital there has been legislation drafted in South Africa that would cause Thungela to have much higher environmental liabilities. It is important to note that this legislation has been in talks since 2015 and has been pushed out every year (now it has been pushed out until summer 2022). Thungela’s CEO seemed very confident that the legislation in its current form will not go into place and Boatman themselves stated that they may have done some double counting but I think it is important to look at the nightmare scenario posted by Boatman and see how the company would not be that bad off in that situation.

Boatman Worst Case

19 Billion Liability - 4 Billion in Coverage by Summer 2022- 5.6 Billion in Leftover Cash Post Dividend Given 8 Billion in Cash Flow = 9.4 Billion Uncovered

While this is not great, by year end 2022 Thungela could have this down to 5-6 billion given coal prices don’t completely collapse within the next 12 months. Further mitigating this Thungela holds the optionality to extend the lifespan of many of its mines.

In this worst case scenario, while not offering 2-3x returns, the company would still be ok.

Conclusion:

Overall, I think this company displays obvious value at current (and prices significantly below current) coal prices and will put this on full display when it reports its H2 results.

Catalysts:

- H2 Earnings and Dividend

Credits and Sources:

- Bafana901 from VIC for getting me interested in the SA scene

- Richard Howe from stockspinoffinvesting who first posted about the idea on Twitter and wrote a great report on Thungela: https://stockspinoffinvesting.com/thungela-resources-buy-the-toxic-waste/

- Short Report: https://theboatmancapital.com/wp-content/uploads/2021/06/Thungela-Resources-Report-6-June-2021.pdf

- Richards Bay Coal Prices: https://www.cmegroup.com/markets/energy/coal/coal-api-4-fob-richards-bay-argus-mccloskey.html#

- https://thungela.s3.eu-west-1.amazonaws.com/downloads/investors/TGA-Int-2021.pdf

Note: I am a barely 18 year old college student with relatively little experience in securities markets and do not encourage anyone to trade under this information whatsoever. This report is merely informational and suggest anyone interested in Thungela follow their own due diligence and come to their own conclusions.